Lecture 1 – Types of businesses and legal registrations in South Africa

1. THE LEGAL TYPES OF BUSINESS IN SOUTH AFRICA

Choosing the legal form of business has significant impact on the complexity of regulatory compliance necessary, the amount of tax you pay the extent of personal liability for debt incurred and whether financial institutions are more or less likely to provide finance. It is therefore important to understand what options exist, and to select the best form for your venture.

Administrative steps for starting a new business:

1. You need to choose a legal entity for your business such as a company or sole proprietorship from which to operate. You need to understand the laws that govern what that legal entity can and cannot do.

2. You need to register with the South African Revenue Services for Value Added Tax (VAT) if applicable, Company Tax (is automatically registered with your entity) and employee tax obligations.

3. Employees need to be registered for unemployment insurance (UIF), workers compensation (WC), and in certain industries to the relevant Industrial Council, a provident fund and a medical aid scheme.

Other than the above, certain businesses such as trading in liquor require permits or licenses. Finally, activities involving cross border trade, i.e. importing and exporting, require permits as well. Acquaint yourself with Common Law, Occupational Safety, Employment Equity, Skills Development, Basic Conditions of Employment, and the Labour Relations Act.

Insure against events external to your business that could put you out of business. Balance the cost of the insurance with the probability of the event occurring.

What is a Legal entity?

When you are born you are a natural person – one that can be touched, fed etc. When you are registered at home affairs you are now also a legal person/entity with an ID number and a record. That record can have many entries such as a license, an income tax record or for some criminal records. Your legal entity cannot be touched or fed but it exists. When you get married some people decide to do it in community of property that means that their legal entities merge to become one, therefore all assets and debts are shared.

When you start a business, you are opening a new legal entity under a new number. There are different types with different rules that apply. Make sure to understand which one will suit you best.

1.1 SOLE PROPRIETORSHIP

It is possible to trade as a sole trader, which implies that the owner of the business operates and assumes all liabilities for his/her business on their own, without the assistance of a partner or other shareholders. A common example of this could be found in most small farmers or doctor’s practices in South Africa, which would be owner-run and operated. It is the simplest form of trading entity and is subject to certain advantages and disadvantages. Your company registration number is your ID number. The business is taxed on your personal tax return as per the statutory tables.

Example: Doctors, small farmers.

Advantages

- The business is simple to organise.

- The owner is free to make decisions.

- The business has a minimum of legal requirements

- The owner receives all the profits.

- The business is easy to discontinue.

Disadvantages

- Unlimited Liability

- No perpetual succession – when you die the business also seizes to exist.

- The proprietor assumes all risk

- Sometimes it is difficult for the proprietor to raise finance

- The proprietor has limited skills upon which to draw

Cost: None (You are already registered with your ID number)

1.2 PARTNERSHIPS

Professionals in practice often form partnerships. Accountants, lawyers and doctors form partnerships so that they can spread their risk and they have a substitute who can stand in should one partner not be able to. A partnership agreement should deal with the following issues: formation, profit sharing arrangements, salaries, banking arrangements, changes of partners, liquidation, responsibilities of partners. A partnership is not allowed more than 20 partners, except in certain instances. All partners are required to include all income from the partnership in their personal tax returns (IT 12) available from the Receiver of Revenue (this only carries the cost of postage – some banks offer assistance with the completion of this form free of charge as a customer service).

Example: Plumbers or some lawyers

Advantages

- Easy to administrate

- Few set-up costs

- It has a definite legal status

- The partners do share risk and rewards, so each partner has a stake in the business

- The partners can stand in for each other

Disadvantages

- Unlimited liability for partners

- No perpetual succession

- No transfer of ownership

- The authority for decisions is divided.

Cost: None, except if you want to use lawyers to set up a partnership agreement.

1.3 CLOSE CORPORATION (CC)

It is no longer possible to form closed corporations; it is worthwhile to have a look at the rules of closed corporations and their advantages and disadvantages. CC’s which are registered may still be purchased but they are becoming increasingly scarce.

RULES OF INCORPORATION

A close corporation is founded by means of a founding statement and cannot exceed 10 members who own and manage the cc. Their interest in the cc must always add up to 100% and be expressed as a percentage.

The close corporation must be profit making in its intentions. This means that a charity cannot incorporate itself as a cc.

It provides the members with limited liability, but the members may offer their creditors personal guarantees that negate a certain amount of the limited liability.

A close corporation is a legal entity on its own. This means that it has a legal persona, and can prosecute and be prosecuted in a court of law.

A Company cannot become a member, as ownership is limited to natural persons. The effect of this is that a cc is never held by a holding company.

The Close Corporations Act No. 69 of 1984 governs a close corporation. Dividends can only be paid if the close corporation is both liquid and solvent (dividends can only be paid if after they have paid, assets exceed liabilities and the business can still pay debts when they fall due).

A close corporation does not need to have an association agreement, but is recommended as it binds members and regulates the internal relationships between members. You can follow the model set out in the amended CC Act, No 17 of 1990. It lays down the voting powers, payments (dividends), member’s rights and duties, meetings, remuneration, benefits, obligations and the extent to which the cc will indemnify members from expenditure incurred for or on its behalf.

The accounting officer is required to submit reliable annual financial records, which agree with the accounting records.

Once the cc has been formed the Receiver of Revenue will ask for the name of your public officer, whose duty is to submit the annual tax returns to the Receiver.

Example: Any business that is relatively small.

Advantages

- It is relatively easy to organise.

- The life of the business is perpetual (i.e. continues after members die).

- The members have limited liability (i.e. they are not personally liable for the business debt).

- The transfer of ownership is easy.

- Fewer legal requirements than a private company.

Disadvantages

- It is subject to special taxation rates.

- The maximum number of members is restricted to ten.

- More legal requirements than a sole proprietorship or partnership

Cost: Currently the price will be determined by the seller.

1.4 COMPANIES

What is the difference between a public and private company?

Public: (Cost: R 1 000 000.00+)

- Shares are offered to the public. (ie JSE – Johannesburg Stock Exchange)

- There is no limitation on maximum shareholders, but there is a minimum of 7.

- There is no limit on the transfer of its shares.

- The word “Limited” will appear at the end of the companies’ name.

- They must make certain information known to the public.

- This type of business is normally very capital intensive.

- There is a minimum of two directors.

- Taxed as a company under companies tax.

E.G.: Anglo American Mining, Spur etc

Advantage:

- To raise capital is very easy as shares are sold to the public.

- Listing on the JSE ensures major international exposure and credibility.

Disadvantage:

- Major reporting duties.

- Major expenses relating to the administration and transparency of the business.

Private: (Cost: R50.00 – Name reservation and R125.00 – Registration)

- Shares are not offered to the public.

- There are a maximum of 50 and a minimum of 1 shareholder.

- There are some restrictions on the transfer of shares.

- The words “(Proprietary) Limited” or “(Pty) Ltd” will appear at the end of the company’s name.

- Does not have to make information available to the public.

- There is a minimum of one director.

- Taxed as a company under companies tax or if it is a small business, turnover tax or small business tax.

E.G.: Most businesses

Advantage:

- Easily transferrable

- Continues even if the owner dies

Disadvantage:

- Can be complicated setup

- Must be taxed according to companies tax/turnover tax

NGO (Non-Governmental Organisation) or a NPO (Non-Profit Organisation):

Section 21 of the Companies Act makes provision for this type of business. It is regarded as a public company and the same applies as above, except there is no share capital. The financial statements at year end may not show a profit, the purpose of the company is usually some charitable cause and the objective therefore is thus not to make money.

Example: Reach for a dream foundation

SUMMARY OF THE ADVANTAGES OF FORMING A COMPANY:

- A public company can issue shares to the public to raise capital.

- Shareholders are not liable for the debts of the company, often negated when shareholders are required to offer personal guarantees.

- As in the case of the close corporation the company has “perpetual succession” (indefinite life-span), which means the business can continue even if the members die.

- The transfer of ownership is easy

- It is easier to raise capital and to expand.

- Efficiency of management is maintained.

- It is adaptable to both small and large business.

Some disadvantages of a private company are:

- It is subject to special taxation rates.

- It is more difficult and expensive to organise than other forms of ownership.

- It is subject to many legal requirements.

1.5 LEGAL REQUIREMENTS FOR YOUR BUSINESS

To avoid problems in your business, make sure that you abide by the following legal- requirements; if you don’t sooner or later you are going to be caught out.You need to do the following:

Contact your local South African Revenue Services (SARS) offices to register:

- As a taxpayer – If you are registering a Company you will also have to register it as a taxpayer. New companies are registered automatically at SARS when registering at CIPC for Income tax – the tax you have to pay on your profits.

- You may also have to register for some if not all of the following:

- Value Added Tax (VAT).

- Employee’s tax. (PAYE)

- Skills development levy. (SDL)

- Trading licences

- Unemployment Insurance Fund (UIF), Workman’s Compensation Insurance (WCA) & Industrial Council (IC)

- Trade mark, copyright, patents & designs

- Note: to register for VAT the SARS might require you to develop a business plan and submit it to their auditors.

1.6 BASIC CONDITIONS OF EMPLOYMENT ACT

You need to keep and display a copy of the Basic Conditions of Employment Act on your premises. This is available from the Department of Labour, posters are available from all major bookstores.

The Wage Determination Act sets out the minimum wage you are allowed to pay your employees. This is obtainable from the Chamber of Commerce or the government printer.

1.7 FORMING A COMPANY:

- It is recommended that you consult a registered accountant or an attorney.

- The Companies Act 71 of 2008 regulates the legal aspects of the company.

- CIPC – Companies and Intellectual Properties Commission have automated the entire process online at www.cipc.co.za

- The first step is to think of 4 possible names for your business, CIPC will test each one from top to bottom the first one that is not taken already will be allocated to your business. If all of them are taken you will have to pay R50 again for the next 4 so be creative and unique.

- You will need the ID, telephone number, email and a postal and residential address for each director.

- For the business you will need an address and a financial year end, it is least complicated when your financial year ends run with the SARS periods ending at the end of February each year.

- It will also ask you how many shares you would like to issue, the current options are 100 or 1000. 1000 Shares enables you to give percentage of shares e.g. 8.5% = 85 shares

- The memorandum and articles of association is generated standard if you register at CIPC

2. THE TAXATION IMPLICATIONS OF OPERATING EACH TYPE OF ENTITY

It is your responsibility as the owner, member or director of a company to ensure that accurate records for tax purposes are maintained.

What is a record?

Any form that contains information. The best way to keep them is in a bookkeeping system for easy access, reporting and continual generation.

E.g. Invoices, bank statements, receipts.

2.1 RECORD KEEPING

If you are involved in a farm business you must keep records that will enable you to prepare complete and accurate tax returns. You may choose a system of record keeping that is suited to the purpose and nature of your business. The records must clearly establish what your income and expenses are. This means that, in addition to your permanent books of account or records, you must maintain all other information that may be required to support the entries on your records and tax returns. Paid accounts, cancelled cheques, etc. that support entries in your records should be filed in an orderly manner and stored in a safe place. For most small businesses, the business chequebook is the prime source for entries in the business records. Be sure to open a separate bank account for your business so that you do not mix your private and business expenses.

2.2 IMPORTANCE OF ACCURATE RECORDS

Accurate records are essential for efficient management. The following reasons demonstrate the need for accurate records.

- Identity source of receipt: You may receive cash or property from many sources. Unless you have records showing the source of your receipts, you may be unable to prove that some are from sources that would make them non-taxable.

- Prevent omission of deductible expenses: Expenses may be overlooked or forgotten when you prepare your tax return, unless you record them at the time they are incurred or paid.

- Establish amounts paid out as salaries or wages: Under normal circumstances amounts paid to employees for services rendered are taxable. In these cases employees’ tax must be deducted from salaries or wages by the person paying such salaries or wages.

- Explain items reported on your income tax return: If the Receiver of Revenue examines your income tax return, you may be asked to explain the items reported. Adequate and complete records are always supported by sales slips, invoices, receipts, bank deposit slips, cancelled cheques and other documents.

- : You are required to keep the books and records of your business available at all times for examination by the Receiver of Revenue. A brief list of the retention periods for documents, records and books is given in the Table below. The retention period commences from the date of the last entry in the particular document, record or book.

Records that you should always keep closeby: (Vendor registration etc)

You are provided with the following table, which summarises the periods a person or a company is required to keep various documents. Read through this table and refer to the next exercise.

| ITEM | RETENTION PERIOD |

| Private Companies Certificate of incorporation Certificate of change of name Memorandum and articles of association Certificate to commence business Minute books |

Indefinite |

| Close Corporations Founding statement Amending founding statement Minute books |

Indefinite |

| Partnerships Partnership agreement |

Indefinite |

| General Annual financial statements Books of account Accounting records including supporting schedules (In terms of Sec 75 (i)(f) of the Income Tax Act) |

4 years |

| Paid cheques | 6 years |

| Tax return and assessments Salary and wage registers Invoices sales and purchases Bank statements and vouchers Stock sheets Sales tax records Other vouchers |

5 years |

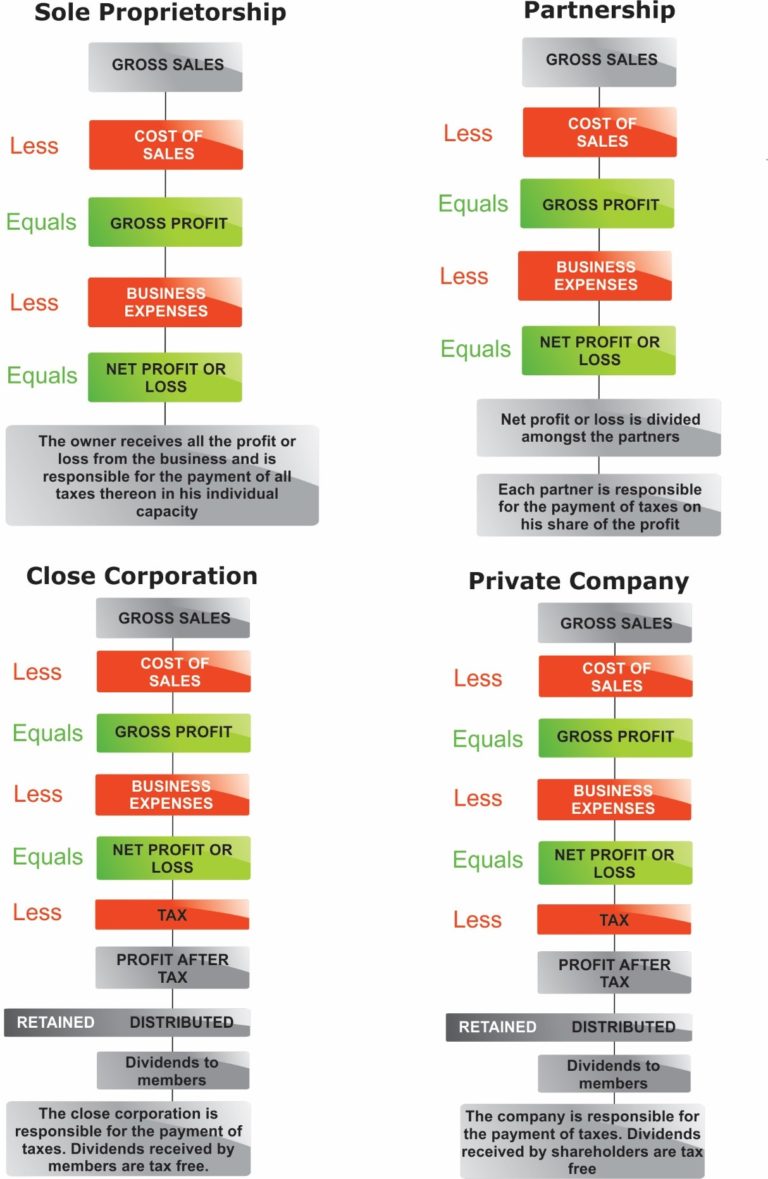

3. COMPARATIVE ACCOUNTING AND TAX STRUCTURES

The following table below illustrates the differences in tax structuring and accounting that you are required to know between the various types of organisations. Read through this table.

4. THE APPLICATION OF THE TYPES OF BUSINESS MODELS

Specific circumstances indicate different types of business models. The model is built up by necessity, from the one-man show, to the public company. It must be said though, at this point, that by far, the close corporation is the most popular model. It allows the limitation of liability for members, while not being too onerous to administer.

THE SOLE TRADER

This business model has very limited use: it can only be applied to a single operator, who would have limited use for additional finance and no need for additional skills input.

THE PARTNERSHIP

Professionals often partner with others in practice. Doctors, lawyers and accountants will form partnerships. It provides the partners with a formal structure and the input of other practicing professionals.

LIMITED COMPANIES

As an enterprise grows, it may incorporate itself as a limited company. This affords it the opportunity to raise external capital, especially through the sale of shares to other companies.

PUBLIC COMPANIES

These are generally the largest operations: they can list on the stock market, raise finance through public share issues and so forth.

5. REGISTRATION WITH THE SOUTH AFRICAN REVENUE SERVICE (SARS)

It is your fiduciary duty as the member or director of a company to ensure that the company is registered as a taxpayer with SARS.You will have to register for the following:

- Income Tax

- Employees Tax

- VAT

The purpose of the registration is to allocate a tax reference number to the company and once a year, when the Annual Financial Statements are calculated, the company must pay the Receiver his due. It is important to note that it is a criminal offence to attempt to get away with not registering. It is an offence to attempt to evade taxes too. Severe fines can be imposed by SARS on the directors or members, and it is possible that the Receiver can have defaulting directors even put in jail.

At this point, it is pertinent to remember: tax evasion is a crime. Tax avoidance, however, is an art and it is a wise person who manages their company in the most tax-efficient manner. The distinction is this: Not declaring taxable income or overstating your expenses is illegal and is classified as tax evasion. Taking advantage of tax breaks and minimising the taxation due to the Receiver is not evasion, it is avoidance. It is beyond the scope of this module to go into some of the more complex avoidance techniques such as deferring taxation, but it is important for any businessperson to be aware that a good tax consultant can save you a lot of money in the long run, by managing the company’s taxes. Consult with an accountant to save money.

A number of forms need to be completed for the Receiver’s purposes. The best thing to do when setting up the company is to consult with a registered accountant who should assist with the process and ensure that your company is properly registered. It is best to just do it upfront and not attempt to play games with the Receiver. There is no getting away from the inevitable.

6. TAXATION RATES

Attached are the current taxation rates for the 2017/2018 budget year. These indicate how much taxation is payable by individuals based on their annual income. Payroll programmes calculate this automatically, it is important to know how this works if you have any employee queries.

| (Annual) INCOME | TAX RATE |

| 0-189 880 | 18% of each R1 |

| 189 881 – 296 540 | 34 178 + 26% of taxable income above 189 880 |

| 296 541 – 410 460 | 61 910 + 31% of taxable income above 296 540 |

| 410 461 – 555 600 | 97 225 + 36% of taxable income above 410 460 |

| 555 601 – 708 310 | 149 475 + 39% of taxable income above 555 600 |

| 708 311 – 1 500 000 1 500 001 and above | 209 032 + 41% of taxable income above 708 310 533 625 + 45% of taxable income above 1 500 000 |

| Primary rebate | R13 635 |

| Secondary rebate 65+ | R7 479 |

| Tertiary rebate 75+ | R2 493 |

Steps to calculate personal income tax:

1. Annualise income

2. Determine the bracket/level/tier

3. Deduct the primary rebate and or other rebates

4. Divide by 12 to get a monthly amount

Example of a tax calculation:

Peter earns R10 000 per month, he is 24 years old

1. R 10 000 x 12 months = R120 000

2. Tax Tier 1 = 120 000 x 18% = R21 600 tax per year

3. – primary rebate R13 635

= R7 965 per year

4. Divided by 12 = R 663.75 Tax per month

Whenever you assist government in their duties they provide tax relief.

E.g. When you have your own medical aid and does not rely on government care you can have an additional amount of tax relief. The same applies to pension and disability insurance.

7. SKILLS DEVELOPMENT LEVY

The skills development levy was introduced by legislation in Skills Development Act, 1998, and the Skills Development Levies Act, 1999. These questions and answers provide information about employers’ obligations in terms of the Skills Development Act, 1998, and the Skills Development Levies Act, 1999; and explain what the levy grant system is all about.

WHAT IS THE PURPOSE OF THIS SCHEME?

The short supply of skilled staff is a serious obstacle to the competitiveness of industry in South Africa. The levy grant scheme aims to expand the knowledge and competencies of the labour force resulting in improvements in employability and productivity. This will be achieved through new approaches to planning for training, learning programmes, incentives and an improved employment service. If you participate fully in the scheme you will reap the benefits of a better skilled and more productive workforce.

WHO MUST PAY THE LEVY?

Every employer in South Africa who:

Is registered with SARS (South African Revenue Services) for PAYE

OR

Has an annual payroll in excess of R500 000.

WHO MUST REGISTER?

Every employer who is liable to pay the levy must register for the payment of the levy with SARS by completing a registration form (form SDL 101 available from all SARS offices).

In order to register, you (the employer) must:

- Obtain a registration form (SDL 101) from any SARS office, if not received by mail,

- choose from a list of registered Sector Education and Training Authorities (SETAs) as indicated in the SETA classification guide provided with the registration form, of 1 (one) SETA most representative of your activities.

WHAT IS A SETA?

SETA stands for Sector Education and Training Authority. 25 SETA’s were established during March 2000 and cover all sectors in South Africa, including government. The members of a SETA include employers, trade unions, government departments and bargaining councils where relevant, from each industrial sector. SETA’s have since been reduced to 21.

IS ANY EMPLOYER EXEMPT FROM THE PAYMENT OF THE LEVY?

Yes. The exemptions are applicable if certain provisions are met. Applications for such exemptions are contained in the SDL 101 form, issued by the Commissioner of SARS, who will ultimately adjudicate whether you qualify for exemption or not.

WHERE (TO WHOM) ARE LEVIES PAYABLE?

Levies are payable to the South African Revenue Service, which acts as a collecting agency for the Department of Labour and SETAs.

HOW ARE LEVIES PAYABLE?

Each month SARS will provide all registered employers with a “Return for remittance” form (SDL 201), which enables you to calculate the amount payable and effect payment.

WHAT AMOUNT IS PAYABLE?

The amount payable will be calculated as follows:

1% (one per cent) of the total amount of remuneration paid to employees. Any prescribed exclusions that are not leviable are subtracted from the total remuneration.

BY WHEN IS THE LEVY PAYABLE?

The levy must be paid over to SARS (after registration), not later than SEVEN days after the end of the month in respect of which the levy is payable, under cover of a EMP 201 return form.

IS THERE ANY INTEREST AND PENALTIES LEVIABLE ON LATE/ NON-PAYMENT OF THE LEVY?

Yes. Interest is payable at the PRESCRIBED RATE (Income Tax Purposes) on late payments. A penalty of 10 PER CENT will be levied on the unpaid amount.

WHAT HAPPENS TO THE LEVIES PAID?

The levies paid to SARS will be deposited into a special fund from where it will be distributed to the relevant SETA as indicated on the registration forms, and the balance will be paid into the National Skills Fund etc. SETAs will in turn pay levy-grants to qualifying employers, while the National Skills Fund will fund skills development projects not within the scope of SETAs. SARS also keeps a percentage for administration of the service.

WHAT IF I AM TRAINING ALREADY?

The levy still has to be paid but you may be eligible for a grant.

CAN I RECOVER ANY OF THIS LEVY PAYMENT BY MEANS OF GRANTS?

In the first year of the levy grant scheme you could recover in grants a minimum of 20% of the levy you paid on condition that you meet all the requirements for the different grants. The details of these requirements were issued in April 2000 by your SETA. Contact your SETA for the current year’s amounts, as these percentages vary from year to year. If you train on scarce skills you can get more back.

WHERE CAN I OBTAIN FURTHER INFORMATION ON MY OBLIGATIONS AS AN EMPLOYER REGARDING LEVY PAYMENTS IN TERMS OF THE SKILLS DEVELOPMENT LEVIES ACT?

The Department of Labour and the SARS have drafted a SDL 10 guideline containing comprehensive details in this regard. This guide was forwarded to all registered employers and is still available from SARS offices.

WHO DO I CONTACT IF I HAVE QUESTIONS ABOUT THE COLLECTION OF THE LEVY IN TERMS OF THE SKILLS DEVELOPMENT LEVIES ACT?

Any SARS office, Department of Labour Head Office and Provincial Offices.

You can get the updated contact details of all SETA’s on google.

8. UNEMPLOYMENT INSURANCE FUND (UIF)

The Unemployment Insurance Act (No 63 of 2001) provides for the Unemployment Insurance Fund (UIF). The UIF works like an insurance against losing a job. If a worker becomes unemployed, the UIF will pay the worker for a period while the worker looks for another job.

The owner of the business, the employer, must register for UIF with SARS. Every month the employer must deduct UIF from the employee’s wages and send the money to the Department of Labour. The employer must also pay something into the UIF Fund.

8.1 HOW TO REGISTER FOR UIF

The employer must register with the Unemployment Insurance Fund in Pretoria. Fill in a form called a UI-8e (EMP201) form and post it to Unemployment Insurance Fund, P O Box É. Pretoria, 0052 or fax it to 012 – 337 1912. This form is available from your local Department of Labour or SARS office or on the Internet at your local Department of Labour or SARS office or on the Internet at www.uif.gov.za.

8.2 WHAT MUST THE EMPLOYER DO EVERY MONTH?

The employer must do five things every month:

- deduct 1% of every employee’s salary

- add another 1% for every employee – this is paid by the employer

- Fill in a form called an EMP 201 for employees who have to pay PAYE, UIF and SDL.

- Forms can be filled in and submitted via www.sarsefiling.co.za

- Payments can also be generated via the efiling channel.

- Submit a file declaring all employees that contributed to UIF or send a UI19 form to Department of Labour.

8.3 WHICH EMPLOYEES PAY UIF

These people cannot claim from the Unemployment Insurance Fund. The employer must not deduct UIF from their salaries:

- People who are not paid a salary, but are paid only for what they make or what they sell. The more they make or sell, the more they earn.

- People working less than 24 hours per month

- Sole traders who are employers

- Someone who does piece work at different premises

- UIF is not calculated on commission

Example:

Sakumsi cuts patterns for dresses. He pays Trevor to sew the pieces together. Trevor works from his house.

Trevor wants to know who is liable for the taxation and UIF payment.

- Sakumsi does not employ Trevor and Sakumsi cannot deduct tax or UIF from the money he pays Trevor

- A working member of a close corporation or working director of a company must now pay UIF. People who earn R17712.00 per year (R17 122.00 per month) or more have to pay UIF, but only up to this ceiling amount. Anyone who earns more than this will only have R177.12 deducted for UIF per month.

- The employer cannot claim money from the UIF if the business fails and has to close down.

9. COMPENSATION FOR OCCUPATIONAL INJURIES AND DISEASES

Workers who get hurt at work, or become sick from diseases caused by their work, can claim Compensation from the Compensation Fund. Employers pay into the Fund.

The Fund does not pay the worker if the accident is the employer’s fault. For example, if the employer, Bobby, knows that he is asking his employee do something dangerous and his employee gets hurt, it is Bobby’s fault. The Fund will not pay the employee. The employee can take Bobby to court.

If a worker gets hurt and can claim from the Fund, she or he can’t take the employer to court. However, there is a legal duty on the part of employers to report any accident at work where a worker has been hurt or injured.

9.1 SOME BASIC CONCEPTS

HOW IS COMPENSATION GOVERNED?

Compensation is regulated by the Compensation for Occupational Injuries and Diseases Act, No. 130 of 1993 (COIDA) as amended by Act 61 of 1997.

THE PURPOSE OF COIDA

The purpose of COIDA is to provide compensation to employees who, in the course of their employment,

- suffer disablement as a result of a work-related injury

- suffer disablement as a result of contracting a work-related disease

- suffer death as a result of a work-related injury or disease.

WHAT IS MEANT BY “COMPENSATION”?

In this guide, as in COIDA, the terms compensation” and “benefits” are used synonymously.

Simply put, compensation includes all the benefits set out in COIDA to which an employee/claimant may become entitled. The payment of compensation depends on the facts of each case. Examples of the types of compensation include, inter alia

- Permanent disablement

- Temporary total disablement

- Temporary partial disablement

- Medical treatment

- A disability pension

- A fatal pension or lump sum payment to dependants

Compensation is always payable in monetary terms. It is aimed at restoring, as far as possible, the pecuniary loss the employee or his dependant/s have suffered following his injury, illness or death in a work-related accident. Compensation does not include a claim for other types of loss or damage, such as property loss or damage, loss of future earnings, loss of amenities of life etc.

Compensation is only payable if the employee has met with an “accident”.

WHAT IS MEANT BY AN “ACCIDENT”?

For the purposes of compensation an employee meets with an “accident” if such accident arises out of and in the course of his employment and results in his personal injury, illness or death.

This concept has been much debated in our law courts for many years and the question of whether an employee has had an accident is still a question of fact. To postulate our court decisions is not within the confines of this guide but in brief the principles which have guided our courts are that an accident:

- Is an unforeseen or unexpected mishap

- Takes place when the employee, in relation to time, place and the control of his employer, is discharging the duties of his contract of employment or matters incidental thereto

- Is causally connected or linked to the employee’s employment

- Results in a personal injury, illness or death.

WHAT IS MEANT BY “DISABLEMENT”?

The term “disablement” does not simply mean that an employee has been hurt or ill because of a work-related injury or disease. The employee must have been seriously disfigured or physically or mentally impaired in some way.

Impairment can be in any form, depending on the nature and extent of the injury or disease. Some more common examples of impairment are:

- The loss of a limb or organ

- The loss of hearing (Noise Induced Hearing Loss)

- Disfigurement by burns or chemicals

- Post-traumatic stress

- Tuberculosis, dermatitis, platinosis

- Para-, tetra- and quadriplegia from spinal cord injuries

- Loss of use of any limb or organ

This list is far from exhaustive. The forms of impairment are in effect more numerous than the parts of the human body.

An employee has also suffered disablement if, as a result of a work-related injury or disease, he is unable for a period of time:

- To perform ANY of the work he was doing before he was injured or contracted a disease

- To perform ALL of the work he was doing before he was injured or contracted a disease or to resume work for less pay.

- It is the effects of the injury or disease, which determine the extent of the two above types of disablement. In the former case the employee cannot work at all because he is, for example, undergoing medical treatment in hospital or otherwise, is convalescing, or the injury or disease is stabilising. In the latter case, the employee can work but can only perform “light duty” or perform another type of work, which carries less remuneration.

9.2 HOW TO REGISTER FOR COMPENSATION

As soon as a business employs someone, the owner of the business must register with the Department of Labour to pay Compensation.

The owner must get a registration form from the Department of Labour. www.dol.gov.za The owner of the business must fill in the form and send it to the Compensation Commissioner in Pretoria.

The Commissioner will send the owner a registration number in about 6 weeks. The Commissioner will also tell the owner of the business how much to pay to the Compensation Fund every year. The owner of the business only pays once a year. The amount depends on how dangerous the work is.

9.3 DOES THE EMPLOYER PAY COMPENSATION FOR ALL EMPLOYEES?

When the employer fills in the registration form, s/he must not write down the names and salaries of employees who cannot claim from the Fund. These employees are:

- employees who earn more than the threshold as determined by the commissioner

- domestic workers who work in private households

- someone who does piecework from a different place is not employed by the business

Example:

Sakumsi cuts patterns for dresses. He pays Trevor to sew the pieces together. Trevor works from his own house. Sakumsi does not employ Trevor and Sakumsi must not pay Compensation for him.

Casual workers who do not work for longer than 3 days in any week for the employer are now protected by COIDA. In other words, their names must be included on the registration form and the employer must pay compensation for them.

9.4 WHAT MUST THE EMPLOYER DO WHEN SOMEONE GETS HURT AT WORK?

The employer must report the accident to the compensation office in Pretoria as soon as possible, but not later than 7 days after the accident. The employer reports the accident by filling in form W.CI.2

10. INDUSTRY SPECIFIC REGISTRATIONS

Certain Industries have specific registrations. If you are establishing a new business, you may want to check whether the following are appropriate.

BARGAINING COUNCIL

Some businesses fall under a council and need to abide by regulations set up by this council. To find out if your business falls under a bargaining council contact your local Department of Labour. There are 59 registered bargaining councils in South Africa.

HEALTH

Consult the Health Department at your local town or city council. If you are going into the food business or you intend opening a nursery school, you need to get the health department to inspect your premises.

SIGNAGE

You need to contact your Local Town or City Council about erecting signs and also about any regulations that apply specifically to your area. You are not allowed to erect signage without the approval of your local council.

MUSIC

Contact SAMRO – South African Music Rights Organisation (011) 489 5000. Every business that plays music for the enjoyment of their staff and customers’ needs to pay an annual levy to SAMRO.

LIQUOR LICENSE

To obtain a liquor license, contact your provincial liquor board or phone Pretoria (012) 3109791. It is a good idea to use the services of a qualified attorney to do this.

IMPORT AND EXPORT

If you are going to import or export or require information on import and export you need to contact the Department of Trade and Industry (DTI).

BAR CODING

Contact the SA Numbering Association (011) 787 4387 if you require barcodes for your products.

PATENTS AND TRADEMARKS

To register a patent or trademark contact the Registrar of Patents, Designs, Trade Marks and Copyright (012) 310 9791.

LOCAL COUNCIL

Speak to your local town or city council to see if you require special permission to operate your business in the area. If you are going to operate your business from home, you will need to obtain permission from your local city or town council as well as your neighbours