Profit and Loss Account

- REASONS FOR THE PROFIT AND LOSS ACCOUNT

The Profit and Loss Account is an account into which all payments and receipts for a business are collected in order to discover if the gains (receipts) are greater than the losses (payments). If the receipts are more than the payments, the business has made a Profit, and if the receipts are less than the payments, the business has made a Loss. The objective of any business is to make a profit, because any business that makes a loss or a series of losses over a period of time cannot carry on as a business and will have to close down. Farming is a business like any other, and the farmer has to make a profit so that he can carry on his business from year to year.

Profit in any business is achieved by exchanging some assets for others of greater value. A farmer buys seed, fertilizer and herbicide and changes these into a crop worth more than his initial investment, so that the farmer shows a profit on the crop. A livestock farmer spends money on buying or raising weaners, on grazing and foodstuffs, and sells mature beef which again, should show profit. The Profit and Loss Account shows the value of these exchanges over a stated period, normally one year. The financial or income tax year covers the period from 1st March to 28th/29th February and many businesses use these dates for the period of their accounts. All businesses including farm businesses must produce a Profit and Loss Account each year so that the amount of their Income Tax can be assessed. In the case of farmers, the figure for profit from the Profit and Loss account is regarded as the farmer’s income for the year and is used to calculate the amount of tax which he must pay for that year. If a farmer, or any business, does not produce a Profit and Loss Account, SARS will make an estimate of the amount earned during the year, and a demand for the tax due on that amount. If the farmer cannot produce figures to show that the assessment of his profit is wrong, he will have to pay the bill. This is the main reason why a Profit and Loss Account is important. It shows the correct amount of the farmer’s income for the year, and his tax bill is based on that figure

The Profit and Loss Account is a financial account which is made up from financial records kept by the farmer during the year. He can either draw up his own accounts or employ an accountant to do the job for him.

- EXAMPLE OF THE PROFIT AND LOSS ACCOUNT

The Profit and Loss below is an example of the possible items in a farm Profit and Loss and will change from farm to farm as indicated in the exercises from lecture 9 to 15.

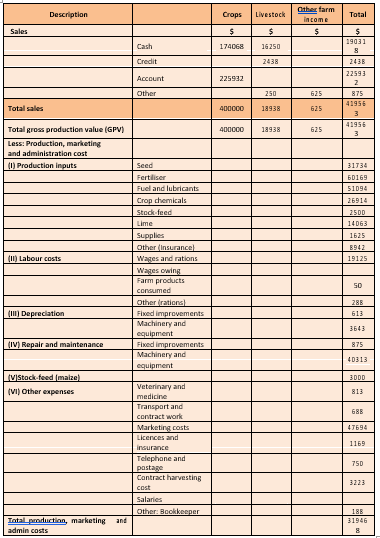

Profit and Loss Account for Lomagundi Farm Pty Ltd; 2011/12 Financial Year

- ANALYSIS OF THE PROFIT AND LOSS STATEMENT

The Heading: Each account must state at the top: the name of the farmer, the farm, and the financialyear to which the account refers. In the case of a farming company, the name of the company will be given (e.g. Lomagundi Farm Pty. Ltd.). The financial year can be shown as in the example, or more detailed – 1st March 2011 to 28 February 2012.

Total Sales: This is the total of the farm income for the year, and provided a profit has been made,this figure is the same as the turnover for the farm for that financial year. In the example, the total receipts and the total turnover for the farm were $419 563 for the 2011/12 financial year. The sales always appear at the top of the account, and in the example the receipts consist of the following items:

Maize Sales: The total of all maize sales during the year together with a value for any maize retainedon the farm for stock feed, rations and maize stocks on the farm at the end of the financial year. Maize sold on account is sold via contracts on the South African Futures Market (SAFEX). The farmer may draw on this account. Maize retained on the farm is valued at the market price less the cost of transport to the nearest SAFEX registered silo. If the market price for maize is $250 a tonne and the cost of transport for that farmer is $10 a ton, he would value any maize retained on the farm at $250 – $10 = $240 a ton. The farmer must keep all payment sheets received from sales to silos, millers or other consumers of maize. A record of all maize used on the farm and any maize in stock at the end of the year must also be kept.

Livestock sales: Sales of livestock made over the year whether they are cash or credit.

Other: Any other receipts that can be classed as farm income. (An example is the dividends paid tothe farmer from shares in an agriculture marketing co-operative such as Senwes. Dividends from private shares held by the farmer are not farm income, but are classed as the farmer’s private income.)

PRODUCTION, MARKETING AND ADMINISTRATION COSTS

This is the total of the farm payments for the year, and all payments appear below sales. In the example, the payments consist of the following items:

Labour costs: This is the total cash paid to all labour, both regular and part time, during the year. Thefarmer should keep a wages book which records all cash payments to all his workers and includes any payments for overtime worked. In addition he should record any rations issued, medicines and education costs paid out on behalf of his labour.

Fuels and lubricants: The cost of diesel fuel, oil and grease used by tractors and machinery such ascombine harvesters, stationary engines, etc. Fuel has to be paid for in cash or by cheque at the time of delivery, and the receipt issued should be kept by the farmer.

Seed: The cost of any seed purchased. In this example, the seed would be seed maize. Any seedsaved from a crop grown on the farm, such as wheat, ground nuts, soya beans etc. should be valued and the amount included as a seed cost.

Fertiliser: The cost of any fertiliser bought and invoiced during the year. Any fertiliser bought theprevious year but still on hand at the beginning of the financial year would appear on last year’s account and would not be included in the current year.

Crop chemicals: All chemicals required for pest and disease control on the maize crops andherbicides bought for use on the farm.

Licences and insurance: All farmers insure their buildings, tractors and equipment against loss ordamage by fire or flood. In addition, some farmers insure their crop against hail damage. This item in the example is the cost of the premiums paid to the farmer’s insurance company. Vehicle licences have also been included in this cost amount.

Marketing costs: this is the money charged as commission by the firms who sell produce for farmers.

It applies to sales of tobacco and sales of cattle by auction.

Transport and contract work: the cost of transporting grain and cattle to the point of sale such as thegrain depot, cattle market or abattoir.

Stock-feed: the cost of both purchased and home grown cattle feed.

Veterinary and medicine: the cost of visits to the farm by a veterinary surgeon, medicines used foranimals and dips during the year

Repair and Maintenance – Fixed improvements: the money spent on repairs and maintenance to allthe buildings and other infrastructure on the farm such as dams.

Repair and maintenance – Machinery and equipment: the money spent on repairs and maintenanceto all the vehicles and other machinery on the farm during the year.

Other or Supplies: any miscellaneous expenses that have not been included in the items above.

Examples might be baling string, wire for fencing repairs, replacement of small tools etc.

Telephone and postage: All costs relating to the telephone, mobile phone and internet that thefarmer uses. Postage costs are also included in this cost item.

Contract harvesting cost: The cost of employing outside harvest contractors to harvest the maizecrop. Many farmers cannot afford their own combine harvesters so they pay contractors to harvest the crop for them.

Accountant or Bookkeeper: The cost of employing an accountant to keep the farm accounts up todate and in order for the financial year.

DEPRECIATION AND INTEREST

Depreciation: This is the cost of writing down assets such as fixed improvements, vehicles andmachinery over a period of years. For vehicles and machinery it is normally 5 years.

Interest paid: the bank will charge interest for money on loans the company has taken, for examplein the form of an overdraft. Other interest items may be incurred from leasing agreements or late payment interest.

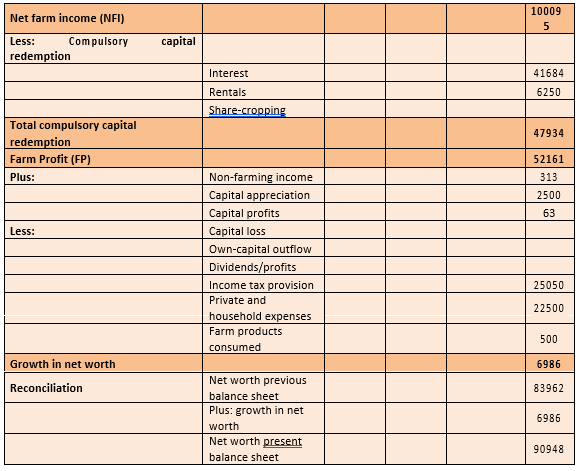

Farm Profit: this is the difference between the Total Sales and the costs for the year, includinginterest. In the example, Total Sales were $419 563 and Costs including interest were $319 468.

| Total Sales | $419 563 | |

| Total Costs | $319 468 | |

| Difference | $100 095 | Farm Profit |

The Farm Profit (FP) should be large enough to cover the following items:

Loan redemption:

The repayment of any loans the farmer might have taken at the start of, or during, the season. In the example the farmer does not have any loan redemption.

Private and household expenses:

The money used by the farmer during the year for his own personal expenses such as food, holidays etc.

Income tax:

The farmer must make provision for his income tax. In the example, the amount, of $25 050 is the farmer’s provision for income tax for the year 1st March 2011 to 28th February 2012. The amount of income tax payable on this sum is calculated by the farmer or farm accountant, and will be paid by the farmer during the 2011/12 financial year. It can happen that a farmer has a very good season and makes a large Net Profit in that financial year, and this makes him liable for a large tax bill. However, the following season is poor, perhaps due to drought; the farmer’s provision for tax will be lower.

The Net Farm Profit is an increase in the capital employed in the farm, and a Net Farm Loss is a decrease in the capital employed in the farm.