Gross Margin Budgeting

INTRODUCTION

Farm Management is an important aspect of modern farming because it emphasises the business side of farming. All farmers, whether they are farming large scale units, small family farms or communal farms, are in the business of food production. At the end of each year they must make a profit, which is used to pay for the following year’s crop or stock cycle and to carry out improvements on the farm. Furthermore, the profit motive is a strong incentive for farmers to make the most of their resources, to produce the maximum amount of food at the lowest cost, and to run efficient, well-kept farms. There is a severe shortage of food in the world today and land has become a very valuable resource that cannot be wasted by poor farming practices. Due to rising populations and the movement of people from the rural areas to the towns and cities no country, particularly in Africa, can afford subsistence farming. Anyone occupying and farming land must produce enough for himself, his family, and a surplus to feed the people in the towns and cities. In order to do this successfully, the farmer must plan his operations carefully so that he can make the best of his basic resources; his land, labour and capital.

The lectures in the Farm Accounts course showed how financial records are kept for the farming business and the way that these records are used to produce two important financial documents each year, namely; the Profit and Loss Account and the Balance Sheet. These reveal a lot about the financial structure of the farm business and the amount of profit and loss made each year by the farming operations, but there is a lot that they do not indicate and because of this, they are not much use for planning future operations on the farm. For example; a farmer grows three crops on his farm; maize, soyabeans and tobacco. The Profit and Loss Account for the farm will tell you the amount he has spent on fertilizer for a year, say $12 000. It does not tell you how much of the fertilizer has been used on each of the crops and you cannot assume that 1/3 of the fertilizer was used on each crop. Maize requires more fertilizer than tobacco, which in turn needs more than soyabeans. The same applies to other items used for the crops; herbicides, packing materials, seed, transport, etc. You cannot allocate these costs to any particular crop just by looking at the Profit and Loss Account. The Gross Margin Budgeting System is designed to overcome this difficulty. By using this system, farmers can allocate their costs to the different enterprises on the farm, find out which of their enterprises are the most profitable, and use this information for planning their future operations.

2. THE GROSS MARGIN SYSTEM

The Gross Margin System is a means of analysing and examining farm records in order to obtain the most useful information for management purposes, ie; information for planning and control of the farm business.

It enables the farmer/manager to determine:

The structure of the farm business

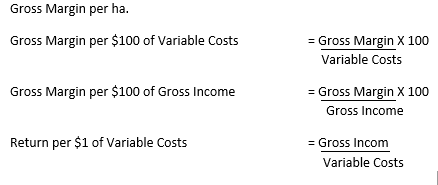

The relative size and importance of the various enterprises on a unit basis, usually per ha for crops and per head or per livestock unit (L.U.) for stock

The varying degrees of profitability of the various enterprises The level of the unproductive overhead costs

Individual enterprise results can be compared with:

Results from previous years on the same farm Results from other farms in the same area

Area and average results published annually by local consultants or the Department of Agriculture

The aim of the farmer/manager should be to use his Gross Margin Budgets to improve future performance on his farm. In farm planning they can be used in the following situations:

As a form of partial budgeting when making comparatively minor changes on the farm; e.g. replacing an area of maize with groundnuts

When considering the purchase of machinery

As an aid to making major changes in an existing business, eg; the introduction of livestock or an area of irrigation

In the planning of a completely new business

Provided that accurate farm records are kept, Gross Margins are easy to calculate.

For any individual enterprise:

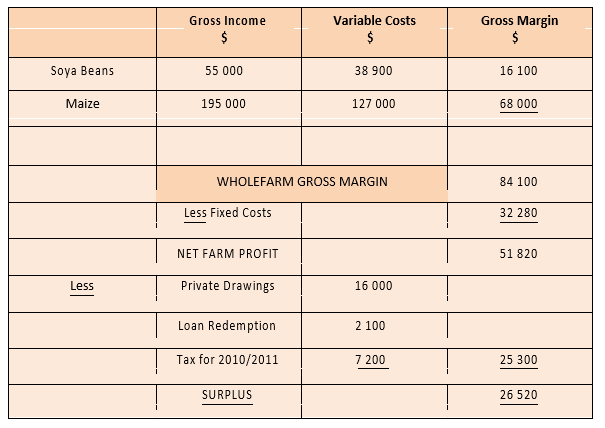

Gross Margin = Gross Income – Variable Costs

The sum of the Gross Margins of all the enterprises on the farm is called the Wholefarm Gross Margin.

Wholefarm Gross Margin – Fixed Costs = Net Farm Profit

VARIABLE COSTS

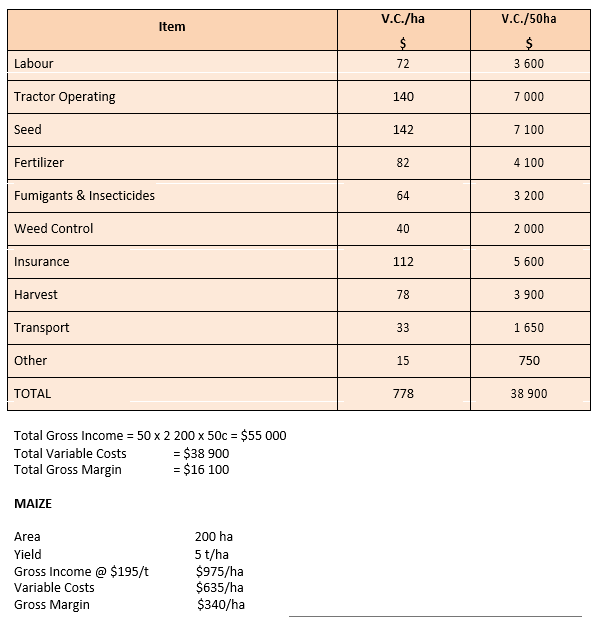

These are costs which can be directly allocated to a particular enterprise, e.g. seed, fertilizer, home grown and purchased feeds, packing, transport etc. Variable costs will rise or fall sharply according to the area of a crop grown or the number of livestock in a unit.

Labour is regarded as a variable cost in Southern Africa because farms employ a lot of labour, and for crops like tobacco, cotton and groundnuts it is the biggest item of costs. Labour costs include wages, bonuses, purchased and home grown rations, housing, schools, medicines and pension fund contributions.

Tractor operating is also a variable cost and includes the costs of fuels and oils, repairs, maintenance, insurance and licences for the tractors and tractor equipment.

FIXED COSTS

These are costs that cannot be allocated to any particular enterprise and remain to be deducted from the Wholefarm Gross Margin. They include such items as accountant’s fees, building maintenance, depreciation, manager’s salaries, unallocated labour and tractor operating costs, interest on loans, etc.

GROSS INCOME

For a cash crop, Gross Income = Income from sales + any insurance compensation.

For a crop, part of which is sold and part retained on the farm for labour rations or livestock feed:

Gross Income = Income from Sales + a value for the crop retained

The value given to the part of the crop retained is the market value less the marketing expenses, (transport, auction fees, levies, etc.)

In the case of a breeding herd, a livestock trading account must be prepared. This will include all sales and purchases of stock and will also show any appreciation/depreciation in herd value during the year. The profit from the livestock trading account will be the G.I. for the enterprise.

In the case of a pen fattening enterprise, where cattle are bought in and sold fat within the same year:

G.I. = Value of stock sold – Value of stock purchased

On a farm where a breeding herd is kept and weaners are pen fattened, a Gross Margin would be calculated for each enterprise. The weaners would be ‘sold’ by the herd to the feeding unit in a paper transaction, at market prices.

For a dairy herd, the G.I. would include the value of all milk, cream and skin disposals, whether as sales or retained on the farm for calves, rations or the farmhouse.

NET FARM PROFIT

Net Farm Profit = Wholefarm Gross Margin – Fixed Costs

This figure is the profit from the year’s trading on the farm.

Surplus

Surplus = Net Farm Profit – Household Expenses, Loan Redemption and Income Tax Payment

This is the money left after all expenses have been met, and can be used by the farmer for private investment or to finance further capital development on the farm.

DEPRECIATION

For farm management purposes, depreciation is charged at a realistic value. Buildings and fixed equipment are normally depreciated at 5% per annum using the Straight Line Method. Tractors are depreciated at 20% and farm machinery at 10% per annum using the Diminishing Balance Method. The reason for this is that buildings and fixed equipment have no resale value whereas tractors and farm machinery will always have some second-hand value, even if this is only scrap value. (See the Farm Accounts Course.)

INTEREST AND REDEMPTION

It is important to remember that interest, which is the charge for borrowing money, is treated as a fixed cost, and redemption, the repayment of the capital borrowed, is deducted from the net farm profit.

LIVESTOCK TRADING ACCOUNT

The Livestock Trading Account shows the difference in values of stock over the trading year together with sales, purchases, births and deaths. Stock are put into classes according to age and sex, and each class is given a value. For farm management purposes these are realistic market values and can vary from year to year. An LTA is calculated for each livestock enterprise on the farm; the beef herd, dairy herd, sheep flock, pig herd, etc. Examples of the LTA are given in the Farm Accounts Course.

TRADING YEAR

For farm management purposes the trading year covers the cropping cycle and runs from 1st October to 30th September, but this can be changed to fit in with a farmer’s specific enterprises and the region in which he is farming.

CO-OPERATIVE STANDARDS

The following standards are used for comparing enterprises:

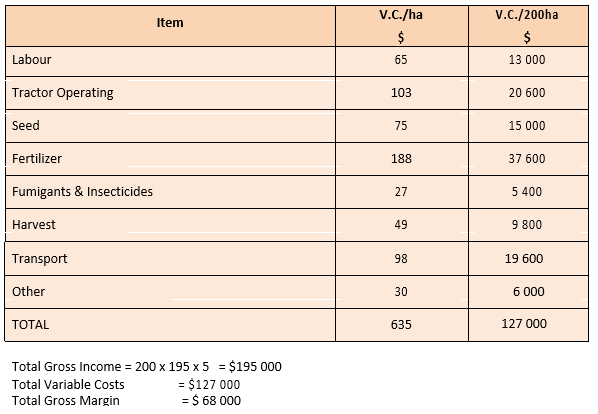

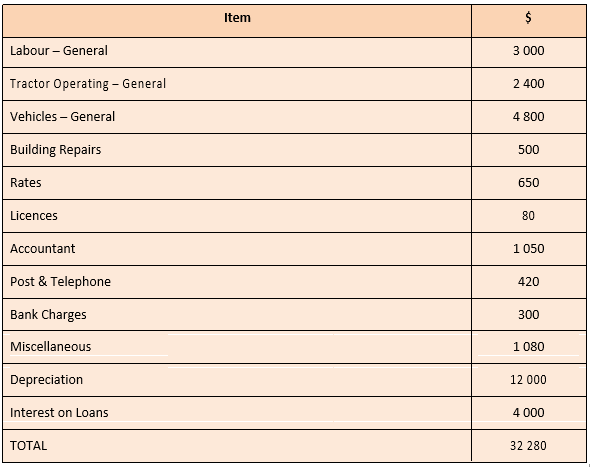

- EXAMPLE OF A GROSS MARGIN BUDGET

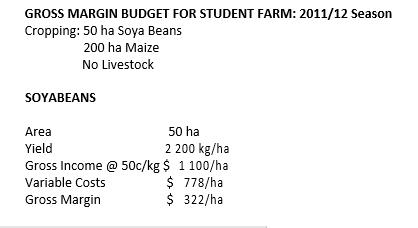

ANNUAL BUDGET FOR STUDENT FARM: 2011/12 Season